Starting a business is often the result of a deep passion and a clear purpose. However, even with the best intentions, many new entrepreneurs find themselves overwhelmed or off track because of early missteps.

While no journey is without challenges, knowing what to watch out for can save both time and energy — and help build a stronger foundation.

Here are five common mistakes many founders make — and how to steer clear of them.

Many entrepreneurs leap into action without a clear roadmap, driven solely by enthusiasm. While energy and passion are powerful, a business without a basic plan can easily drift off course.

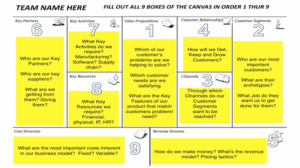

A simple, evolving business plan doesn’t need to be complicated — but it should address:

The plan is not only a tool for potential investors — it’s a guide for the entrepreneurs themselves. Keep it fluid, review it regularly, and adjust it as the business landscape evolves.

Above, you can see the overall sequence of thoughts that you need to put into your business plan. A business plan is more than just a document. It serves as your guide first for yourself, then for your team, and to attract potential investors. To add to the above, the following are a few additional points to consider.

A brilliant idea is only as good as its fit for the market. Skipping the step of validating your concept can result in products or services that don’t resonate with real customers.

To avoid this:

Understanding your audience is essential — not only for development, but also for effective communication and informed pricing.

Cash flow issues are one of the top reasons startups fail to survive. Without a grasp of income, expenses, and buffers, a business can quickly run into trouble.

Practical steps include:

Being proactive with finances helps reduce stress and supports informed decision-making.

Entrepreneurs often wear every hat — marketing, finance, operations — and it can be both exhausting and isolating.

Rather than doing everything yourself:

Support systems are not a luxury — they’re a necessity. Sharing challenges and ideas helps keep momentum and offers fresh insight.

An excellent service or product means little if no one knows about it. Without a strategy for visibility, even the best offerings can remain hidden.

Founders should:

Brand visibility is not about being everywhere — it’s about being intentional and consistent where it matters most.

Final Thoughts

Starting a business can be one of the most fulfilling journeys — but it’s also one that demands resilience, clarity, and learning by doing. Avoiding these five common pitfalls won’t make the path linear, but it will set a healthier rhythm for sustainable growth.

A final reminder for those stepping into entrepreneurship:

You don’t have to get it perfect. You have to get started — and stay open to learning.

Hulya Kurt is an Executive Coach championing women’s economic empowerment. She is committed to making a societal impact, inspiring the younger generation, and contributing to a better, more inclusive world.

+ 3 more

Master coach guiding professionals to career clarity, confidence, and meaningful leadership growth.